A lot of parents in The Woodlands start with the same question. They get a bonus, a commission check, a distribution from a business, or uneven self-employment income, and then they ask: what income counts for child support in Texas?

That confusion is normal. Texas child support usually doesn't turn on one paycheck. It turns on net resources, and that can include far more than salary alone. In Montgomery County cases, that becomes especially important when a parent works in sales, owns a business, receives performance pay, or has income that rises and falls during the year.

If you're also sorting out post-divorce benefits, health coverage can affect the broader financial picture too. A practical starting point is understanding COBRA and ACA for divorcees, especially when support, medical coverage, and monthly cash flow all have to work together.

This article is general information, not legal advice. Texas child support decisions depend on the facts of your case, your documents, and the court handling your matter.

Starting with the Basics of Texas Child Support

Texas child support starts with a broad financial question, not a narrow payroll question. The court wants to know what money is available to a parent after the deductions the law allows. That is why people who focus only on wages often miss important parts of the analysis.

In plain English, what income counts for child support in Texas usually includes more than base pay. If your compensation includes overtime, bonuses, commissions, side income, business income, rental income, or recurring money from other sources, those items may matter. In higher-income households in The Woodlands, that's often where disputes begin.

Why this catches parents off guard

Many parents assume child support is based on gross pay or take-home pay from one job. It usually isn't that simple. A parent can look underpaid on a paycheck stub and still have substantial financial resources once other income streams are included.

That matters on both sides. The parent paying support may feel like irregular income is being overstated. The parent receiving support may believe the other side is showing only a salary while leaving out their total income.

Practical rule: If money comes in regularly or meaningfully affects your household finances, assume it may become part of the child support discussion.

The issue isn't just income. It's proof.

The legal fight is often less about labels and more about records. Courts and lawyers look for tax returns, pay statements, year-end compensation documents, bank records, business statements, and other evidence that shows a reliable financial picture over time.

That is why bonus-heavy and self-employment cases take more work. A single month can mislead the court in either direction.

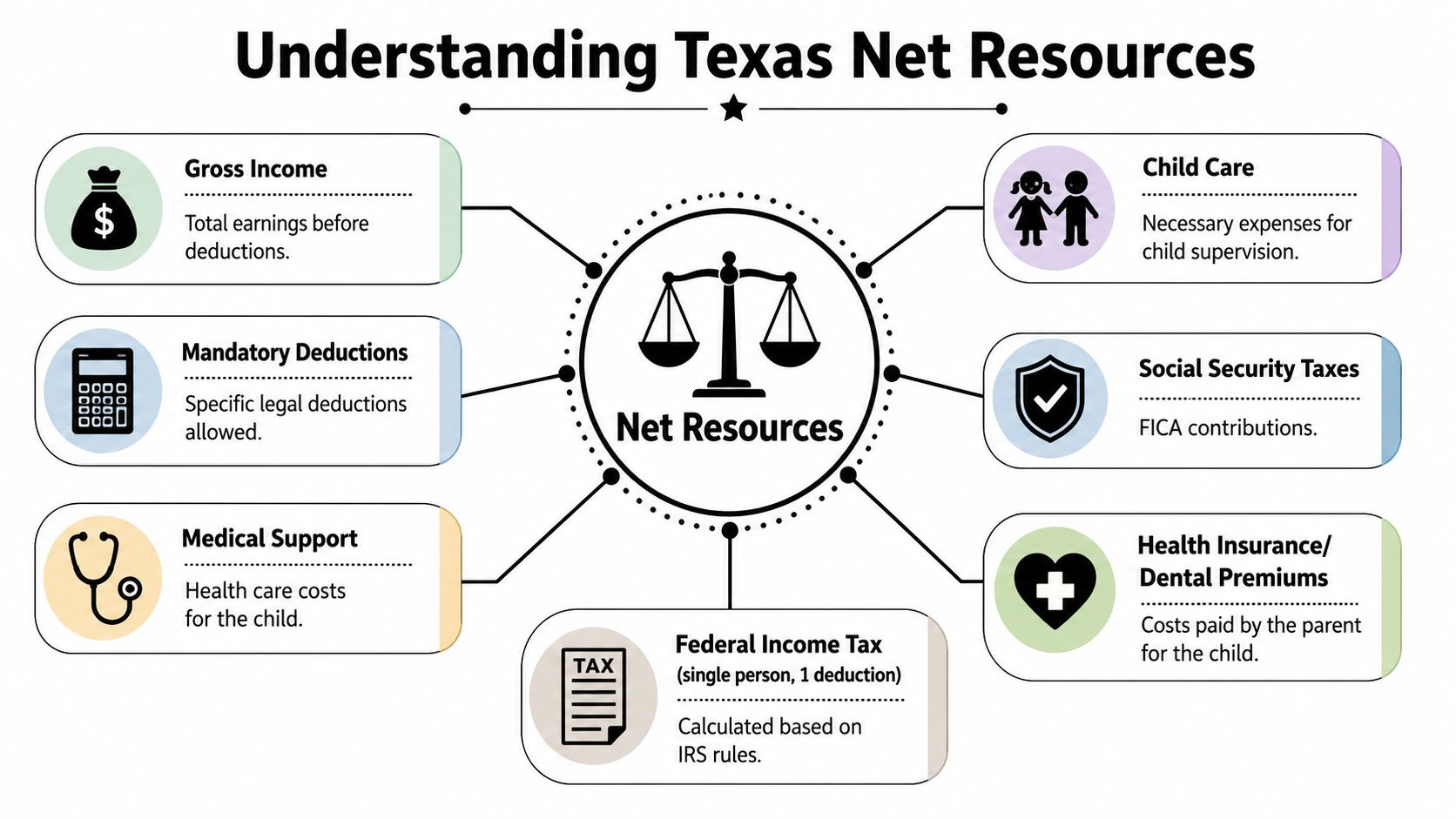

The Foundation of Texas Child Support Net Resources

A Woodlands parent may bring me a pay stub showing a moderate salary, then mention a year-end bonus, restricted stock, a side business, and rental income from a second property. That is usually the moment the case starts to make more sense. Texas child support turns on net resources, which is the court's way of measuring the parent's real financial capacity, not just the number listed as base pay.

The starting point is broad. Courts look at money and benefits a parent receives, then subtract only the deductions the law allows. In practice, that matters because a clean payroll record can hide a much larger financial picture. It also matters in the other direction. A parent with a strong compensation package on paper may have an unusually low year and need records that show the full context.

Texas Law Help explains the basic rule this way: child support is based on monthly net resources rather than simple gross wages, and the analysis can include money from many sources, including wages, commissions, bonuses, self-employment income, rental income, retirement income, and some benefits, as discussed in Texas Law Help's explanation of child support and lower incomes.

In Montgomery County, this issue shows up constantly in higher-income cases. Sales executives may receive a modest base salary and a large quarterly bonus. Business owners may write off legitimate expenses that reduce taxable income, but the court will still ask what money is available for support. Parents in construction, energy, medicine, and finance often have compensation that rises and falls during the year, which makes a single pay period a poor measure of actual resources.

That is why these cases are document-driven.

Judges want a reliable picture over time. For a W-2 employee, that may mean year-to-date pay information, prior tax returns, and bonus history. For a self-employed parent, it often means bank records, profit-and-loss statements, general ledgers, business account statements, and proof of which expenses are real business costs versus personal spending run through the company.

Parents also need to separate net resources from monthly stress. Mortgage payments, private school tuition, credit card balances, club memberships, and car notes may be real obligations, but they do not automatically reduce child support the way people expect. The court's focus stays on income and recognized deductions, not the lifestyle a parent built around that income.

Benefits can create confusion too. If you are dealing with job loss or a benefit-based income stream, it helps to understand whether child support comes out of unemployment benefits in Texas, because those payments are often treated differently from ordinary wages but still matter to the support analysis.

The practical takeaway is simple. In a bonus-heavy or self-employment case, the parent who brings organized records usually has the stronger position. The parent who relies on a single paycheck stub, or a tax return without backup, often leaves the court to fill in the blanks. In Montgomery County, that can lead to an income finding that does not match how either side wanted the case framed.

Common Income Sources Counted for Child Support

A parent in The Woodlands may have a base salary that looks modest on paper, then earn a large year-end bonus, quarterly commissions, partnership distributions, or cash flow from a closely held business. That is where child support cases stop being simple payroll exercises. In Montgomery County, the court looks past the job title and asks a harder question: what money is available to support the child?

For some families, the answer is straightforward. For others, especially high-income households and self-employment cases, income comes in layers. A paycheck is only one layer.

What is commonly included

Texas courts generally cast a wide net when identifying income for child support. Common sources include:

- Salary and wages from regular employment

- Commissions and bonuses, including performance pay that comes in unevenly

- Overtime and tips if they are a real and recurring part of earnings

- Self-employment income from a business, contract work, consulting, or side work

- Rental income from investment or inherited property

- Interest, dividends, and other investment returns

- Retirement or pension income that is being received

- Unemployment or disability benefits in many cases

- Gifts, prizes, and other recurring funds received

- Non-cash compensation if it provides a measurable financial benefit

The dispute is often not whether a category can count. The primary fight is whether the amount claimed reflects reality.

That matters in Montgomery County. A sales executive may argue that a bonus was unusual and should be ignored. The other parent may show a three-year pattern proving the opposite. A business owner may call payments distributions or reimbursements. If those payments regularly cover personal living costs, the label alone will not carry much weight.

What is commonly excluded or treated differently

Some money does not count the same way, and some items require a closer legal analysis before they are included. SSI is a common example that is treated differently from ordinary earnings or business income.

Benefits also create confusion. Parents often mix up whether a payment can be withheld for support with whether it counts as a financial resource in the first place. If that issue is part of your case, this explanation of whether child support comes out of unemployment benefits in Texas helps sort out the difference.

Income inclusions vs exclusions for Texas child support

| Typically Included in Net Resources | Typically Excluded from Net Resources |

|---|---|

| Wages and salary | SSI |

| Overtime | Money that is not truly available to the parent as a resource |

| Tips | Items requiring separate legal analysis before inclusion |

| Bonuses | |

| Commissions | |

| Self-employment profits | |

| Rental income | |

| Interest and dividends | |

| Retirement or pension income | |

| Unemployment benefits | |

| Disability benefits | |

| Gifts and prizes | |

| Non-cash compensation at fair market value |

Do not rely on labels. A draw, shareholder distribution, company-paid vehicle, or reimbursement can become an income issue if the records show it reduces personal expenses or puts money in the parent's hands.

Where parents get into trouble

The most common mistake is underreporting by focusing only on wages. I see that often with bonus-heavy compensation packages and closely held businesses. The second mistake is treating personal spending, business write-offs, or debt payments as automatic reductions to support income. Courts usually separate tax strategy from actual ability to pay.

A better approach is to identify every source of money first, then test each one against the records. In a self-employment case, that often means the court is deciding not just what a parent earned, but what the parent chose to call income.

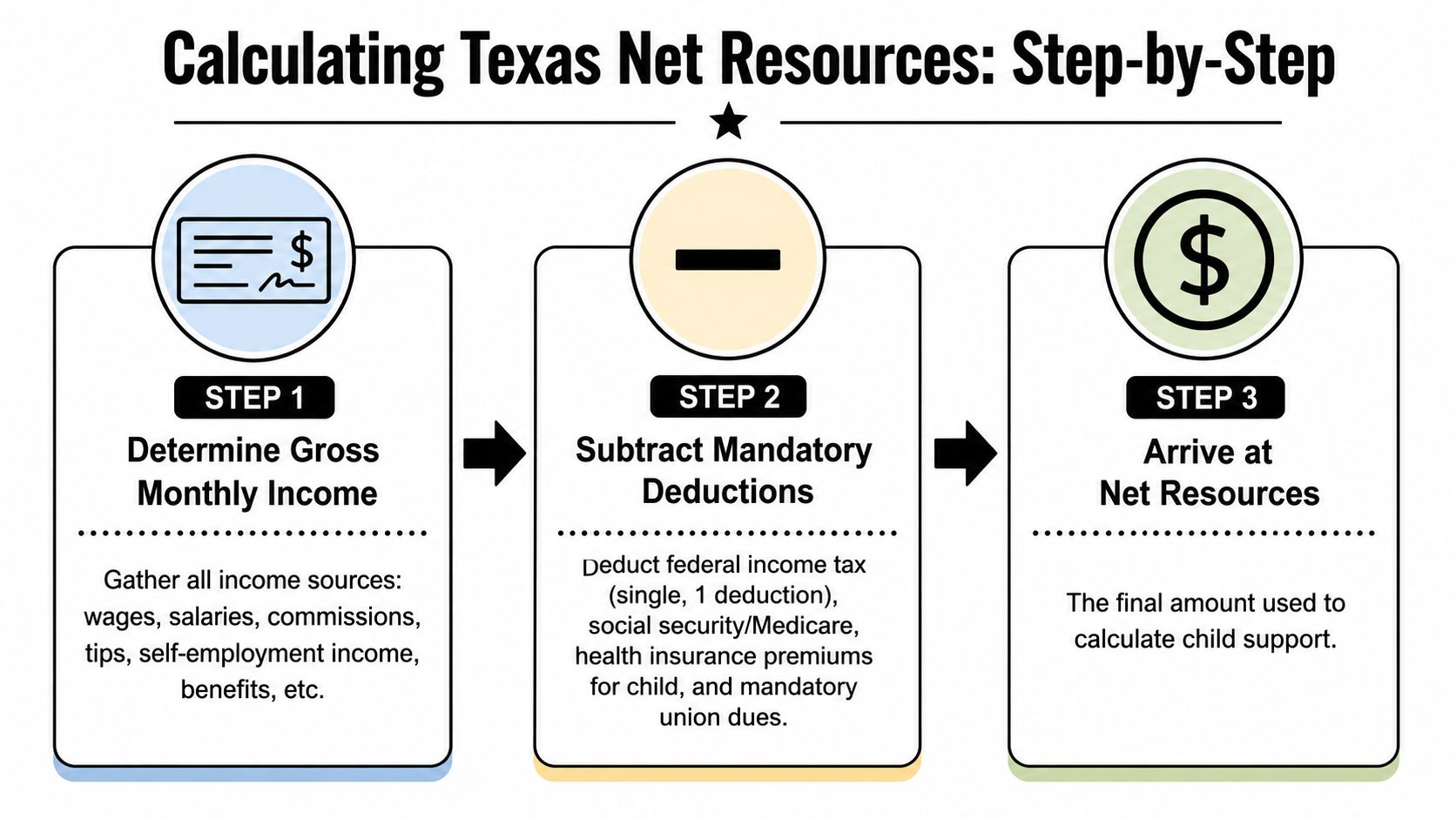

How Net Resources Are Calculated in Texas

A parent in The Woodlands may have a solid base salary on paper, but the child support calculation often turns on money that does not arrive in a flat paycheck. Annual bonuses, quarterly commissions, restricted stock payouts, owner draws, and uneven business income can change the result more than the salary line does. Texas still requires the court to convert that reality into one monthly net-resources figure.

After that number is established, the guideline percentages are applied up to the current cap. The Texas Attorney General's Texas child support calculator reflects the standard framework and percentages used in most cases.

The calculation sequence

Texas courts generally work through three steps:

Determine gross income from the sources that count.

That can include wages, incentive compensation, self-employment income, investment income, and other financial benefits that function as actual resources.Subtract the deductions Texas law permits.

Common examples include certain taxes, union dues, and qualifying health insurance costs for the child.Calculate monthly net resources.

That is the figure used for the guideline percentage.

For parents trying to estimate a starting point, this explanation of child support guidelines in Montgomery County is useful. In practice, though, estimates break down quickly when compensation changes from month to month.

What makes the math harder in real cases

The formula sounds straightforward. The dispute usually is not.

In a salary-only case, the documents may line up neatly. In a bonus-heavy or self-employment case, the court has to decide what period fairly represents earning capacity, whether a payment was recurring, and whether claimed business deductions reduced personal ability to pay support. That is why one paystub rarely settles the issue in Montgomery County.

A good set of records often includes tax returns, year-end pay summaries, payroll history, bank statements, profit and loss statements, and documents showing who paid personal expenses. Courts want a monthly number, but the proof often comes from a much longer financial timeline.

The cap matters in higher-income cases

The cap is important in higher-income households, especially in parts of Montgomery County where compensation packages are tied to performance. The guideline formula does not automatically keep increasing without limit. Once net resources rise above the cap, the argument often shifts to whether guideline support alone is appropriate or whether the evidence supports a different amount based on the child's proven needs and the parent's actual resources.

That distinction matters. A high earner does not automatically owe the same amount as every other parent above the cap, and a parent with volatile income is not helped by pulling one favorable month out of context.

A practical example

Suppose a parent works in sales and receives a moderate base salary plus large commissions paid at irregular times during the year. Using one strong quarter can overstate support. Using one weak month can understate it. Courts usually look for a pattern that better reflects what the parent had available over time.

The same problem appears in self-employment cases. A business owner may report low taxable income while the business covers vehicle costs, travel, meals, or other expenses that reduce personal spending. Those items are often where the child support fight begins.

Bottom line: In a fluctuating-income case, the main job is establishing a defensible monthly net-resources figure before the guideline percentage is applied.

Complex Income and Common Disputes in Montgomery County

The hardest child support cases in Montgomery County usually aren't about whether wages count. They are about how to accurately measure uneven income. That's common in The Woodlands, where many parents work on commission, receive annual bonuses, own businesses, or have income tied to investments and distributions.

Bonus and commission cases

A bonus can be real income even if it doesn't arrive every month. The argument is usually about treatment, not existence. One side may say the bonus is part of the parent's regular compensation. The other may argue it was unusual, nonrecurring, or too uncertain to treat as monthly income.

What works in these cases is context:

- Compensation history over more than one pay period

- Employment agreements showing how incentive pay works

- Year-end statements that confirm whether the bonus is routine

- Bank records showing when money was received

What doesn't work is isolating one favorable month and pretending it represents the whole year.

Self-employment and business owner disputes

Self-employment cases are document-heavy for a reason. Business owners may show modest taxable income while still enjoying substantial cash flow, expense coverage, or distributions. On the other hand, some businesses do have legitimate swings, and not every gross receipt is spendable income.

That is why these cases often turn on credibility and paper trails. Judges usually want records that separate true business expenses from personal spending that has been run through the business.

Useful records often include:

- Tax returns

- Profit and loss statements

- General ledgers

- Business bank statements

- Credit card statements

- Loan applications or financial statements, if they exist

Parents in higher-income disputes often need a more focused look at high-income child support issues in Montgomery County, especially when the case involves ownership interests or complex compensation.

A business can reduce taxable income on paper and still leave a parent with meaningful resources for child support purposes. That tension drives many of these cases.

Imputed income and underemployment

Another recurring fight is whether support should be based on actual current earnings or earning capacity. Texas guidance notes that intentionally staying unemployed or underemployed can lead to additional support, a point discussed in this overview of Texas child support issues.

In practice, "imputed income" arguments usually show up when a parent's reported earnings drop sharply and the other side believes the drop is self-created. That can happen after a job change, business restructuring, reduced hours, or a claimed slowdown in a self-owned company.

What judges usually want to see

A parent claiming lower actual income should be prepared to show why. Helpful evidence may include:

- Medical records or work restrictions, if health is part of the story

- Job search records if the parent lost employment

- Business records showing a real downturn

- Prior earnings history to explain whether current income is temporary or part of a longer trend

A parent asking the court to impute income needs more than suspicion. The stronger argument usually points to prior earnings, qualifications, work history, and signs that the current income picture isn't reliable.

In contested cases, lawyers often build the case backward. They compare tax returns, bank deposits, payroll documents, and lifestyle evidence to test whether the reported number makes sense. That is often more persuasive than broad accusations.

Real-World Scenario A Woodlands Sales Executive's Bonus

A Woodlands sales executive can look overpaid on one paycheck and underpaid on the next.

David lives in Alden Bridge and works on a compensation plan that is common in Montgomery County. His salary is steady, but a large share of his income arrives through an annual bonus tied to production. During the divorce, the other parent sees that bonus hit the account and assumes support should be recalculated from that single payment.

Courts usually look at the pattern, not the drama of one deposit. If income rises and falls with annual incentives, stock-based compensation, commissions, or deferred payouts, the central issue is what David earns over time. In practice, that often means pulling several years of pay records, bonus statements, W-2s, and bank deposits to see whether the bonus is a true outlier or part of a recurring compensation structure.

That distinction matters in high-income cases from The Woodlands, where employers often shift compensation away from straight salary. A parent may report a modest monthly base pay while receiving large quarterly or year-end incentive money. If the record shows those payments happen regularly, the court is more likely to treat them as part of ongoing resources rather than a one-time windfall.

The case can get harder if David also receives reimbursements, car allowances, restricted stock, or compensation through a closely held business. Then the dispute is no longer just about a bonus. It becomes a proof problem. Which payments are income, which are business-related, and which claimed deductions are real?

Older support orders can complicate the analysis too. If David's current earnings are substantially different from the income used in the existing order, counsel should compare the old order, the current compensation records, and the applicable guideline limits in effect at the time the court rules. In some cases, the issue is a straightforward guideline update. In others, the main fight is whether the other parent can prove resources above the guideline cap and seek support beyond the presumptive amount.

This is why bonus cases are document cases. The parent asking for more support needs more than one year-end pay stub. The parent resisting an inflated number needs more than a claim that the bonus was unusual. Clean records usually decide whether the court sees a temporary spike, a reliable income stream, or an effort to understate true financial resources.

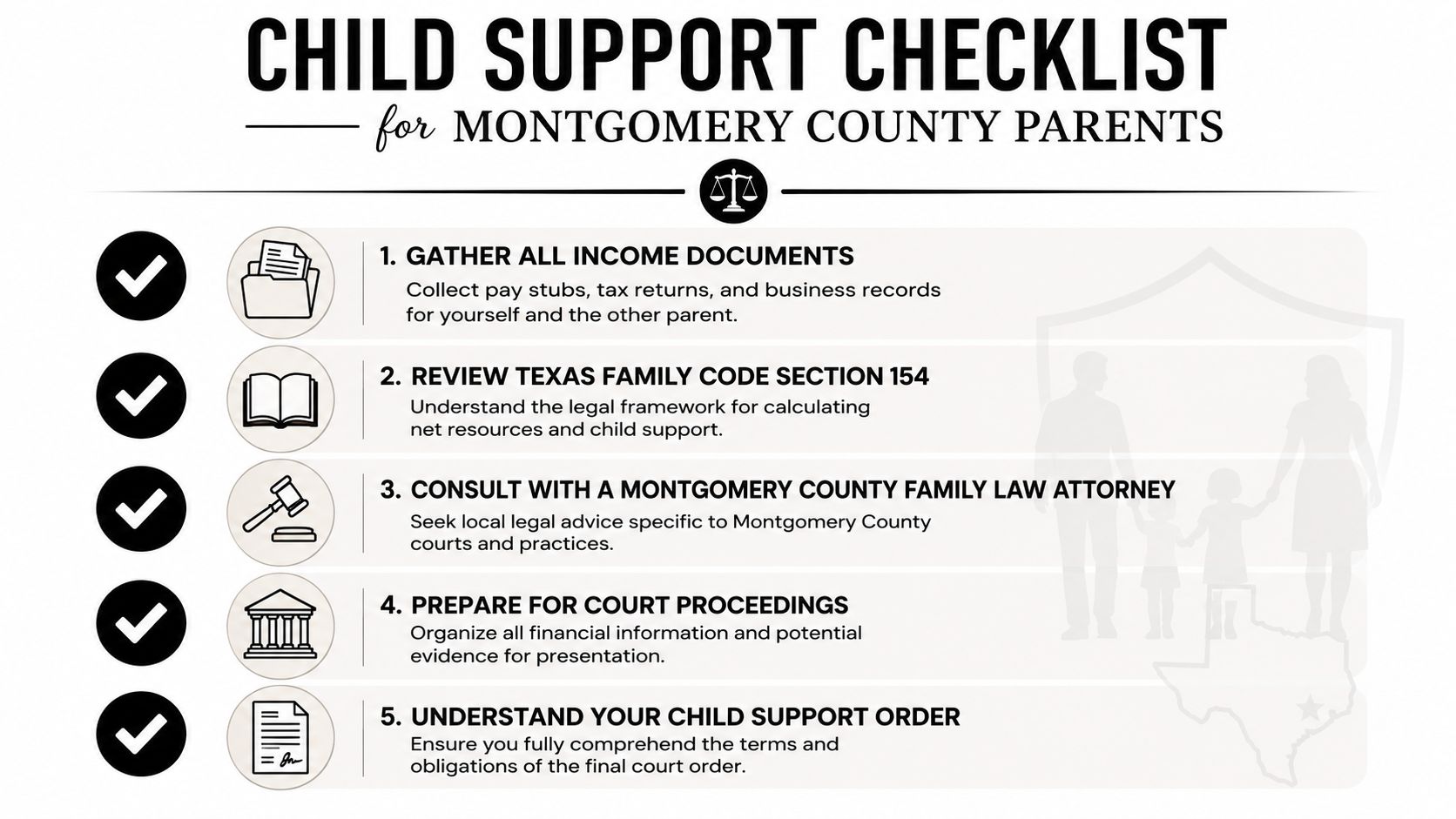

What to Do Next A Checklist for Parents

A parent walks into my office with two pay stubs and a rough estimate of last year's bonus. The other parent arrives with bank deposits, prior tax returns, and a spreadsheet showing irregular payments over 18 months. The second parent usually starts in a stronger position because child support disputes are won with records, not assumptions.

What to do next

- Collect records by category and by month. Gather pay stubs, bonus and commission statements, tax returns, K-1s, profit and loss statements, business account records, personal bank statements, retirement income records, and proof of side income. In fluctuating-income cases, a clean timeline matters as much as the records themselves.

- Build a twelve-month, and sometimes twenty-four-month, income picture. One strong quarter can overstate income. One weak month can understate it. Parents in The Woodlands with bonus-heavy compensation or self-employment income should expect the court to look for patterns.

- Flag the hard issues early. Identify reimbursements, car allowances, stock compensation, owner draws, claimed business expenses, recent income drops, cash payments, and any reason the other side may argue income should be imputed.

- Compare the current order to current finances. If support was set years ago, pull the old order and the records used back then if you have them. The question is not only what you earn now, but whether the change is large enough, and well-documented enough, to justify modifying the order.

- Separate business spending from personal spending. Self-employed parents often lose credibility when personal expenses run through a business account. If the books are messy, fix that before mediation or a hearing if possible.

- Use online estimates carefully. They can help with straightforward W-2 income. They are far less useful when compensation includes bonuses, commissions, restricted stock, partnership income, or disputed deductions.

- Prepare your explanation, not just your paperwork. A judge or mediator will want to know why income rose, why it fell, whether a bonus is recurring, and whether claimed expenses are necessary to produce income.

- Get local guidance if the numbers are contested. A Montgomery County family law attorney can test the reliability of the financial records, frame the proof, and spot where an income claim is overstated or understated. One local option is The Law Office of Bryan Fagan, which handles family law matters in The Woodlands and surrounding Montgomery County communities.

Bring records in chronological order. That simple step often shortens the consultation and makes the support analysis more accurate.

This article is not legal advice. Child support outcomes depend on the facts, the available proof, and the court handling your case.

If you need help sorting out bonus income, self-employment records, or a disputed child support calculation in The Woodlands or Montgomery County, consider scheduling a consultation. A focused review of the financial records can clarify what income is likely to count, what proof is missing, and whether a modification or contested hearing makes sense.