If you're facing divorce in The Woodlands, the number that keeps you up at night often isn't the mortgage. It's the retirement balance.

That surprise hits a lot of people in places like Sterling Ridge, Alden Bridge, and Creekside Park. They assumed the house was the big asset. Then they look at the 401(k), IRA, pension, deferred compensation, or employer stock plan and realize those accounts may represent years of work and most of the future they thought was settled.

That is where divorce with retirement accounts the woodlands becomes different from a basic property division case. These assets don't just have a balance. They have tax consequences, plan rules, vesting schedules, and a paper trail that can help you or hurt you.

Texas law gives you a framework, but the framework alone doesn't protect you. You need records, a workable division plan, and the right court orders. If you miss the details, you can lose separate property claims, trigger avoidable taxes, or accept a settlement that looks fair on paper but is not fair in real life.

Your Retirement and Your Divorce The Woodlands Reality

A common local scenario looks like this. A couple in The Woodlands has been married for years. One spouse worked for an energy company and built a large 401(k), plus some stock-based compensation. The other spouse may have a pension, an IRA, or time out of the workforce while raising children. When divorce starts, both people ask the same question in different ways: What happens to retirement now?

The answer usually isn't simple. Retirement accounts often contain a mix of property earned before marriage and property earned during marriage. Some accounts can be divided with a court order. Others require special drafting and careful coordination with the plan administrator. In high-asset Montgomery County divorces, the retirement piece can shape the entire settlement.

A short real-world example

Take a couple in Sterling Ridge divorcing after a long marriage. The husband has a 401(k) that started before the wedding and kept growing during the marriage. The wife has a smaller IRA and expects to rely heavily on retirement assets after divorce. They both assumed they would just split the account and move on.

That approach usually misses the core issues.

The first question is whether part of that 401(k) is separate property because it existed before marriage. The next question is how much of the later growth belongs to that separate portion. Then comes the division method. Is the account split directly? Is another asset traded against it? Does a QDRO need to be prepared? If there are company stock units in the package, that analysis gets harder.

Retirement division is often where a reasonable divorce settlement either comes together or falls apart.

In The Woodlands, I see people focus on the current balance and ignore the history of the account. That mistake can be expensive. The better approach is to slow down, gather records, identify what part is community property, and divide it in a way that preserves value instead of eroding it.

Understanding Community Property and Your Retirement Nest Egg

A retirement account can be partly yours and partly part of the marital estate at the same time. That point surprises a lot of people in The Woodlands, especially in marriages where one spouse brought substantial savings into the relationship and kept contributing for years afterward.

Texas law starts with a presumption. Under the Texas Family Code property rules, property on hand at the time of divorce is generally presumed to be community property unless a spouse proves a separate-property claim. For retirement assets, that means the court does not solely look at whose name is on the account. The court looks at timing, source of contributions, and whether the records support a clear division between pre-marriage and marital portions.

What counts as community and what counts as separate

Community property usually includes earnings and assets acquired during the marriage.

Separate property usually includes property owned before marriage, plus certain gifts and inheritances.

Applied to retirement accounts, the rule is practical. Contributions made before marriage are generally separate property. Contributions made during marriage are usually community property. Growth tied to each portion may follow that characterization, which is why a 401(k), pension, or deferred compensation account often has to be examined line by line instead of treated as one lump sum.

That issue becomes more important in high-net-worth divorces. A senior executive in The Woodlands may have a base 401(k), employer match, deferred bonuses, stock options, and RSUs earned on different schedules. Some awards may have been granted during the marriage but vest later. Others may be tied to work performed partly before marriage or after separation. Those details affect value and division.

Why this matters in real life

Mistakes in this part of the case can follow you for years.

I often see spouses focus on the current balance because it feels concrete. Texas courts focus on characterization first. If you skip that step, you can end up offering away separate property, fighting over funds that were never divisible, or accepting a settlement that looks even on paper but is uneven after taxes and transfer rules are applied.

Practical rule: Treat retirement accounts differently from cash in the bank. Ownership, tax treatment, and division rules are different.

Why account title does not decide ownership

One spouse's name on the statement does not settle the issue. In Texas, title is only part of the picture. The better question is when the asset was earned and whether the history of the account can be proven with records.

That is one reason mixed finances create problems during divorce. If spouses have spent years combining income and expenses through a joint account for married couples, they often assume retirement assets work the same way. They do not. Retirement accounts follow their own plan rules, tax rules, and property rules, and those differences matter in settlement talks.

For a broader local framework, this overview of property division in The Woodlands divorce cases explains how Montgomery County courts approach marital versus separate property.

The Critical Task of Tracing Your Separate Property

If you claim part of a retirement account is separate property, the burden is on you to prove it.

That point gets missed all the time. Under Texas community property law, the account holder must show which part of a 401(k) is separate and which part is community. If clear proof like pre-marriage statements isn't available, courts can presume the entire account is community property and subject to 50/50 division, as explained in this discussion of splitting a 401(k) in Texas divorce.

What tracing actually means

Tracing is the process of proving the history of the account.

For a retirement account, that usually means showing:

- The balance on the date of marriage: This is the starting point for a separate property claim.

- Statements over time: Annual or periodic statements help show contributions and growth.

- Current balance and plan details: The court needs a reliable present-day picture.

- Any rollovers or transfers: If funds moved from one account to another, the paper trail has to follow them.

If the account existed before marriage, the original balance on the marriage date is usually the anchor. Growth tied directly to that pre-marital balance may also matter, but only if the documentation supports it.

The documents that matter most

People often tell me they can probably get the records later. Sometimes they can. Sometimes they can't.

Start here:

Pre-marriage account statement

This is the single most important record for many separate property claims.Statement close to the wedding date

If the exact date statement isn't available, get the closest available statement before and after.Year-end statements during the marriage

These help identify contributions, gains, losses, and plan changes.Current statement

This shows the account value now and helps frame settlement discussions.Plan summaries and employment records

These can clarify matching contributions, vesting, and account type.

If you're missing the statement from the date of marriage, don't give up. But don't assume the court will fill in the blanks for you.

What goes wrong in real cases

The most common tracing failures are practical, not legal.

One spouse rolled an old 401(k) into a new employer plan and lost the original statement. Or the parties switched financial advisors several times. Or nobody saved the annual statements because everything was online. Or a spouse assumes testimony alone will be enough to prove what part was theirs before marriage.

Usually, it won't be.

Texas courts work from evidence, not memory. The more years involved, the more important the paper trail becomes. In long marriages common in The Woodlands, retirement accounts often pass through multiple employers, multiple custodians, and several investment shifts. That doesn't make tracing impossible. It does make early document collection essential.

A practical way to approach tracing

Use a simple file system. Separate records by account, then by year.

Create folders for:

- 401(k) and pension records

- IRA records

- Rollovers and transfer confirmations

- Employer compensation documents

- Tax forms tied to distributions or account changes

Then build a timeline. Marriage date. Job changes. Rollovers. Plan conversions. Major contributions. Loans, if any. You are trying to tell a clean financial story backed by records.

In some cases, lawyers bring in financial experts to help with valuation and tracing. That isn't necessary in every case, but in a high-asset divorce it can make the difference between preserving a valid separate property claim and losing it.

Valuing and Dividing Different Types of Retirement Accounts

Not all retirement assets work the same way. A 401(k) is not a pension. An IRA is not an RSU plan. If you treat them as interchangeable, the settlement can look balanced while giving each spouse very different real value.

The basic comparison

| Account Type | How It's Valued | Primary Division Method | Key Consideration |

|---|---|---|---|

| 401(k) or similar defined contribution plan | Usually by account balance on the agreed valuation date | Often divided by court order, commonly a QDRO for employer plans | Loans, gains or losses after valuation, and matching contributions can affect the final split |

| IRA | Usually by account balance | Often divided through the divorce decree and transfer paperwork | Tax character matters. Traditional and Roth dollars are not always equal in after-tax value |

| Pension or defined benefit plan | Often valued by projected future benefit rather than a simple current balance | Usually divided through a specialized order tied to the plan | Timing, survivor benefits, and payment options matter as much as the headline benefit |

401(k)s and other defined contribution plans

These are usually the easiest retirement accounts to understand and the easiest to misunderstand.

The current statement gives you a balance, but that doesn't answer every divorce question. You still need to know what portion is marital, whether any amount is separate property, and whether the division will be stated as a percentage or as a fixed amount tied to a certain date.

A common trade-off comes up in settlement talks. One spouse wants to keep the 401(k) and offset it by giving the other spouse more equity in the house or more cash from another account. That can work. But it only works if both sides account for taxes, liquidity, and long-term growth. A house and a retirement account are not interchangeable dollar for dollar.

IRAs

IRAs can look simpler because they are individual accounts, but they still raise real issues.

The first issue is classification. If an IRA was funded before marriage, tracing still matters. The second issue is tax treatment. A traditional IRA and a Roth IRA may show similar balances, but they don't have the same future tax consequences. In negotiation, that difference should be discussed directly, not brushed aside.

An IRA division also needs careful drafting in the decree and transfer paperwork. People sometimes assume they can move funds informally after divorce. That is where avoidable tax trouble begins.

Pensions

Pensions are where many clients need the most explanation.

A pension usually promises a future benefit rather than showing a pile of money in an account you can divide today. That means the value question is harder. In some cases, the spouses divide the future stream of payments. In others, they try to offset the pension against other assets.

If pensions are new to you, a plain-English guide on understanding pension benefits can help you get oriented before you negotiate.

A pension settlement can fail even when the math looks fine. The problem is often timing, survivor rights, or the payment option selected at retirement.

A short scenario from local practice

Consider a couple in Montgomery County. One spouse worked in education and has a pension. The other worked for a private employer in the energy sector and built a strong 401(k). On paper, the couple thinks they can "trade" the pension for the 401(k) and avoid the hassle of dividing both.

Sometimes that works. Sometimes it doesn't.

The pension may not pay for years. It may include election choices at retirement that affect value. The 401(k) has a visible balance today but may carry market risk and tax consequences. If one spouse needs near-term stability and the other is willing to accept more future uncertainty, the trade might make sense. If both spouses just want a clean split without really valuing what they are giving up, it can be a bad deal.

What usually works and what usually doesn't

What tends to work:

- Use a clear valuation date: Ambiguity creates post-decree disputes.

- Match the division method to the account type: Pension language should not be copied from a 401(k) order.

- Account for taxes: Equal balances do not always mean equal value.

What tends not to work:

- Swapping assets without analysis: Cash, equity, pensions, and retirement plans behave differently.

- Ignoring post-separation gains and losses: Those details matter in drafting.

- Assuming every account needs the same order: Some do, some don't.

The right approach is usually account-specific. That sounds obvious, but it gets lost quickly once settlement pressure builds.

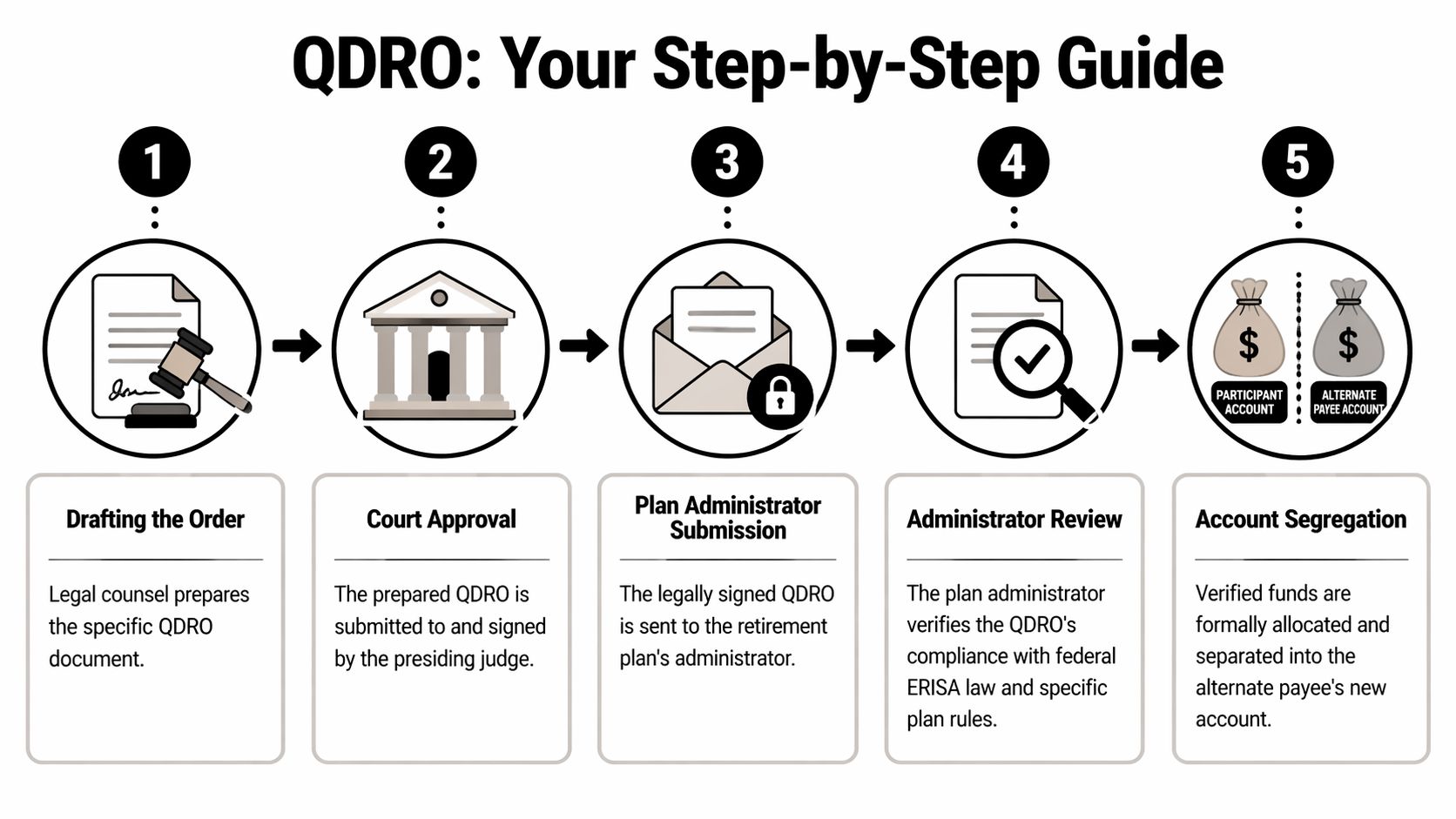

The QDRO A Step-by-Step Guide for The Woodlands Residents

For many employer-sponsored retirement plans, the most important document in the entire case is the Qualified Domestic Relations Order, or QDRO.

Without it, a divorce decree alone may not be enough to divide the plan properly. A properly used QDRO can allow a transfer without the usual 10% early withdrawal penalty, even if the receiving spouse is under age 59½, as noted in this discussion of QDRO use in The Woodlands divorce cases. That same source notes that in contested high-asset Montgomery County cases, retirement actuaries may charge $500–$2,000 and forensic accountants may charge $5,000–$25,000+.

Early in the process, it helps to see the workflow visually.

What a QDRO does

A QDRO tells the plan administrator how to divide the retirement plan consistent with the divorce orders and federal plan rules.

That matters because the court can award a share of the plan in the divorce, but the plan administrator still needs a compliant order before the plan will separate and transfer funds.

The five practical steps

Draft the order carefully

The language has to match the divorce terms and the plan's requirements. Generic forms often create problems.Get the judge's signature

The QDRO usually needs court approval after the substantive property terms are settled.Send it to the plan administrator

At this point, many people stall out. They assume the signed order finishes the job. It doesn't.Wait for the administrator's review

The plan reviews the order for compliance. If the wording is off, the order may be rejected and need revision.Confirm the account segregation

Do not assume the transfer happened just because the order was approved. Get confirmation.

Later in the process, some people find it useful to watch a short visual overview before reviewing the actual order language.

What people get wrong about QDROs

A few mistakes show up repeatedly:

- Waiting too long: The divorce is final, everyone is exhausted, and the QDRO gets pushed aside.

- Using vague settlement language: If the decree doesn't clearly describe the division, drafting the order gets harder.

- Not checking the plan's model language: Many administrators have preferred terms or sample provisions.

- Failing to follow through after court approval: The administrator's acceptance is the finish line, not the judge's signature.

The signed decree is not the end of the retirement division process. It is often the midpoint.

When a QDRO is worth extra attention

QDRO issues become especially serious in gray divorce and in high-asset cases. Retirement accounts may be the largest single asset. There is also less time to rebuild after mistakes.

If the marital estate includes multiple plans, old employer accounts, or unusual benefit elections, careful drafting matters even more. This is one area where cutting corners often costs more later. The Law Office of Bryan Fagan handles divorce and property division matters in The Woodlands, including retirement-related orders used in local family court practice.

Beyond the 401k Complex Assets in High-Net-Worth Divorces

Many online articles stop at 401(k)s and IRAs. That leaves out a major issue in The Woodlands.

For executives, physicians, engineers, and corporate employees in Montgomery County, the harder assets may be stock options, RSUs, deferred compensation, and non-qualified plans. These don't fit neatly into the same framework as a standard retirement account.

Why these assets get overlooked

They are less familiar, and the paperwork is often worse.

A 401(k) statement usually gives a balance. Stock awards and deferred compensation plans may involve grant dates, vesting schedules, forfeiture risks, tax timing, and company-specific restrictions. In The Woodlands' high-net-worth divorces, employer stock options and deferred compensation are often overlooked. Texas courts treat them as community property if earned during marriage, but valuation requires complex models. Roughly 25% of high-asset divorces in Montgomery County involve executive compensation, according to this Montgomery County QDRO and executive compensation discussion.

For readers dealing with a broader estate of business and investment assets, this page on high-asset divorce in The Woodlands is a useful companion.

The practical issue isn't just value

The central question is often not "What is it worth today?"

The better questions are:

- When was it earned

- When does it vest

- What part relates to work performed during the marriage

- What tax event happens later

- Should it be divided now or when it pays out

Those are different questions from the ones asked with a standard IRA.

What works better in these cases

A few approaches tend to produce better outcomes:

- Read the plan documents closely: Grant agreements and deferred compensation documents matter.

- Separate earning period from payout date: An asset can vest later but still be tied in part to the marriage.

- Use precise settlement language: Future vesting events create disputes if the decree is vague.

- Coordinate with tax planning: A good-looking division can turn bad after vesting taxes hit.

Some of the most expensive mistakes in high-net-worth divorce come from treating executive compensation like ordinary cash.

What usually doesn't work is forcing these assets into a generic "split everything equally" formula. They may require a deferred division, a contingent formula, or a negotiated buyout based on risk. In other words, the right answer often depends on the structure of the compensation itself.

What to Do Next Your Practical Checklist

If you're dealing with retirement accounts in a Montgomery County divorce, act early and stay organized. Delay is expensive.

Your checklist

- Gather statements now: Pull retirement statements from before marriage, around the marriage date, during the marriage, and current statements.

- List every account: Include 401(k)s, IRAs, pensions, annuities, stock options, RSUs, and deferred compensation.

- Don't move money casually: Avoid withdrawals, loans, or informal transfers unless your lawyer has reviewed the consequences.

- Check beneficiary designations: Don't assume divorce alone fixes estate planning or retirement beneficiary issues. The Texas Estates Code can become relevant after divorce, but plan-specific rules still matter.

- Ask for plan documents early: Summary plan descriptions, award agreements, and administrator contact information help prevent drafting delays.

- Review support issues too: Retirement division often overlaps with cash-flow concerns, and this overview of spousal maintenance in The Woodlands can help you spot related issues.

- Get local legal help before settlement language is final: Bad wording in the decree can create avoidable QDRO and enforcement problems later.

A few clear don'ts

- Don't assume your name on the account decides ownership

- Don't assume equal balances mean equal value

- Don't assume the decree alone completes the transfer

- Don't assume missing records won't matter

This article is not legal advice. It is general information about Texas divorce and retirement issues, focused on The Woodlands and Montgomery County. Your facts, your account history, and your plan documents will control the analysis.

If you're trying to protect retirement savings, preserve a separate property claim, or negotiate a workable division, a consultation with local family law counsel can save time and prevent costly mistakes.

Frequently Asked Questions About Retirement and Divorce in Texas

Can my spouse cash out a 401(k) before the divorce is final

They may try, but that does not mean they should or that the court will ignore it. Temporary orders, standing orders, and final property division can all affect how that conduct is handled. If you're worried, raise it with your lawyer immediately and gather the most recent statements.

What if my ex dies before I receive my share of a pension

That depends heavily on the plan terms and the wording of the order. Survivor benefits, beneficiary elections, and plan-specific options matter. This is one reason pension drafting should be done carefully and not copied from a generic template.

Do I have to take my share of the retirement account right away

Not always. The answer depends on the type of account, the plan's rules, the decree language, and the transfer order. In some cases, funds can be rolled into another retirement account. In others, the plan controls what options are available.

If you're sorting through divorce with retirement accounts in The Woodlands, a focused legal review can help you identify separate property issues, evaluate division options, and avoid preventable tax mistakes. The attorneys at The Law Office of Bryan Fagan work with families in The Woodlands and Montgomery County on divorce, property division, and high-asset cases. If you'd like to discuss your situation, you can schedule a consultation.