If you're divorcing in The Woodlands, there's a good chance the house isn't your biggest asset. The 401(k) is.

That surprises a lot of people. They may live in Panther Creek, Alden Bridge, or Sterling Ridge, have a mortgage, two cars, and a long work history, then realize the retirement account built over the marriage may matter more than anything else on the balance sheet. That is especially true in long marriages and for spouses nearing retirement.

Dividing a 401(k) isn't like splitting a checking account. Texas treats property division under community property rules, but a retirement account has layers. Some money may be separate property. Some may be community property. The gains tied to each portion matter. Then there is the QDRO, the court order required to divide many employer retirement plans correctly.

Clients also need to know how this works locally. In Montgomery County, details matter. The paperwork has to match the plan. The order has to be approved in the right sequence. And if you choose a bad valuation method early, you can spend the rest of the case trying to undo the damage.

This article is for informational purposes only. It is not legal advice and does not create an attorney-client relationship.

Your 401k Is a Major Asset in a Woodlands Divorce

A common first meeting starts the same way. A couple from The Woodlands, Texas comes in focused on the house, then we lay out the balance sheet and the 401(k) is worth more than the equity in the home.

That changes the strategy.

In Montgomery County, retirement accounts often drive the property division discussion long before anyone talks about final paperwork. A 401(k) can affect whether it makes sense to keep the house, whether one spouse needs a cash offset, and whether a proposed settlement is fair after taxes, market movement, and plan rules are considered. Generic divorce articles usually miss that point. They treat the account like a single number on a statement. Real cases are more complicated.

The account balance also does not answer the valuation question by itself. One of the most common mistakes I see is the subtraction method. People take the balance on the date of marriage, subtract it from the current balance, and assume the difference is community property. That shortcut can produce the wrong result because it ignores how gains and losses attach to separate and community portions over time. If that error gets built into temporary negotiations, fixing it later can be expensive.

Local procedure matters too. Judges in Montgomery County expect the numbers in the inventory, decree, and later retirement orders to line up. If the account is a major asset, sloppiness early in the case creates settlement problems later. Missing statements, unclear payroll records, and bad drafting can turn a solvable property issue into a fight over tracing and post-decree corrections.

A 401(k) division also has to be evaluated against the rest of the estate. I often tell clients not to compare a dollar in home equity to a dollar in a retirement plan as if they are identical. They are not. Home equity may give present-day flexibility. A 401(k) may carry tax consequences, plan restrictions, and timing issues. The better question is which trade serves your goals. Keep the house, preserve retirement, reduce debt, or create liquidity.

If you are reviewing the bigger picture of property division in The Woodlands divorce, the 401(k) should be analyzed early and carefully.

The biggest early mistake is assuming one account statement gives you one clean answer. In a Woodlands divorce, the history of the 401(k), and how you prove that history, often matters as much as the balance itself.

Is Your 401k Separate or Community Property

In Texas, property division starts with the community property framework. Under Texas Family Code § 3.002, community property generally includes property acquired by either spouse during marriage. Under Texas Family Code § 7.001, the court divides the community estate in a manner that is "just and right."

That sounds straightforward until you apply it to a retirement account.

What part of the account is actually divisible

The short answer is this: only the portion earned during the marriage, plus the growth tied to that marital portion, is typically subject to division.

If the account already existed before the wedding, the balance on the date of marriage may be separate property. But that doesn't mean the whole account stays separate. Contributions made during the marriage, employer matches during the marriage, and the investment growth associated with those marital contributions may all become part of the community estate.

The burden is on the employee spouse to prove what portion is separate. If that proof is weak, the court may treat more of the account as community property than you expected.

Why the subtraction method causes trouble

A lot of people try to solve this with simple math. They look at the account balance on the date of marriage, subtract it from today's balance, and call the difference community property. That is often called the subtraction method.

It sounds clean. It often isn't accurate.

As discussed in this Woodlands-focused review of dividing a 401(k), the subtraction method can fail because it doesn't account for different growth rates between pre-marital separate funds and marital contributions. That source gives an example in which an account had $100,000 at marriage, later grew to $500,000, and also received $200,000 in marital contributions. If separate property grew at 8% annually while community portions grew at 6%, a simple subtraction can overstate the divisible amount. The same source states that 35% of contested cases require expert valuation to correct this issue and notes a projected 22% rise in QDRO disputes in 2025 after market volatility.

Practical rule: If the account existed before marriage and grew for years during the marriage, don't assume subtraction is good enough.

Better ways to trace the account

In many Montgomery County cases, lawyers and financial experts look to more precise tracing methods, including the field method, and in some disputes they may discuss approaches such as the time rule or coventry formula adjustments when the facts support it.

The point isn't the label. The point is accuracy.

A better tracing process usually requires:

- Statements from the date of marriage forward

- Records of each contribution source, including employee deferrals and employer matches

- Evidence of account performance over time

- A clear valuation date agreed to by the parties or used by the court

If one spouse walks into mediation with a single recent statement and a rough estimate, that spouse is negotiating from a weak position. If the other spouse has complete records and a defensible tracing analysis, the discussion changes fast.

What Montgomery County judges care about

Judges deciding property disputes don't reward guesswork. They look for credible proof that supports a "just and right" division under Texas Family Code § 7.001.

That is why account history matters more than assumptions. In a high-asset case from Sterling Ridge or Creekside, the difference between proper tracing and bad tracing can affect the overall property division, settlement advantage, and whether the parties choose an offset instead of a split.

A simple comparison shows the issue:

| Approach | What it does well | What it misses |

|---|---|---|

| Subtraction method | Fast and easy to explain | Often ignores separate growth and can overstate community property |

| Field method | Tracks contributions, matches, and gains more carefully | Requires better records and more analysis |

| Forensic tracing | Strongest for disputed or high-value accounts | Adds cost and usually makes sense only when the numbers justify it |

When clients ask what works, the answer is consistent. Good records work. Plan documents work. Careful tracing works. Shortcuts usually don't.

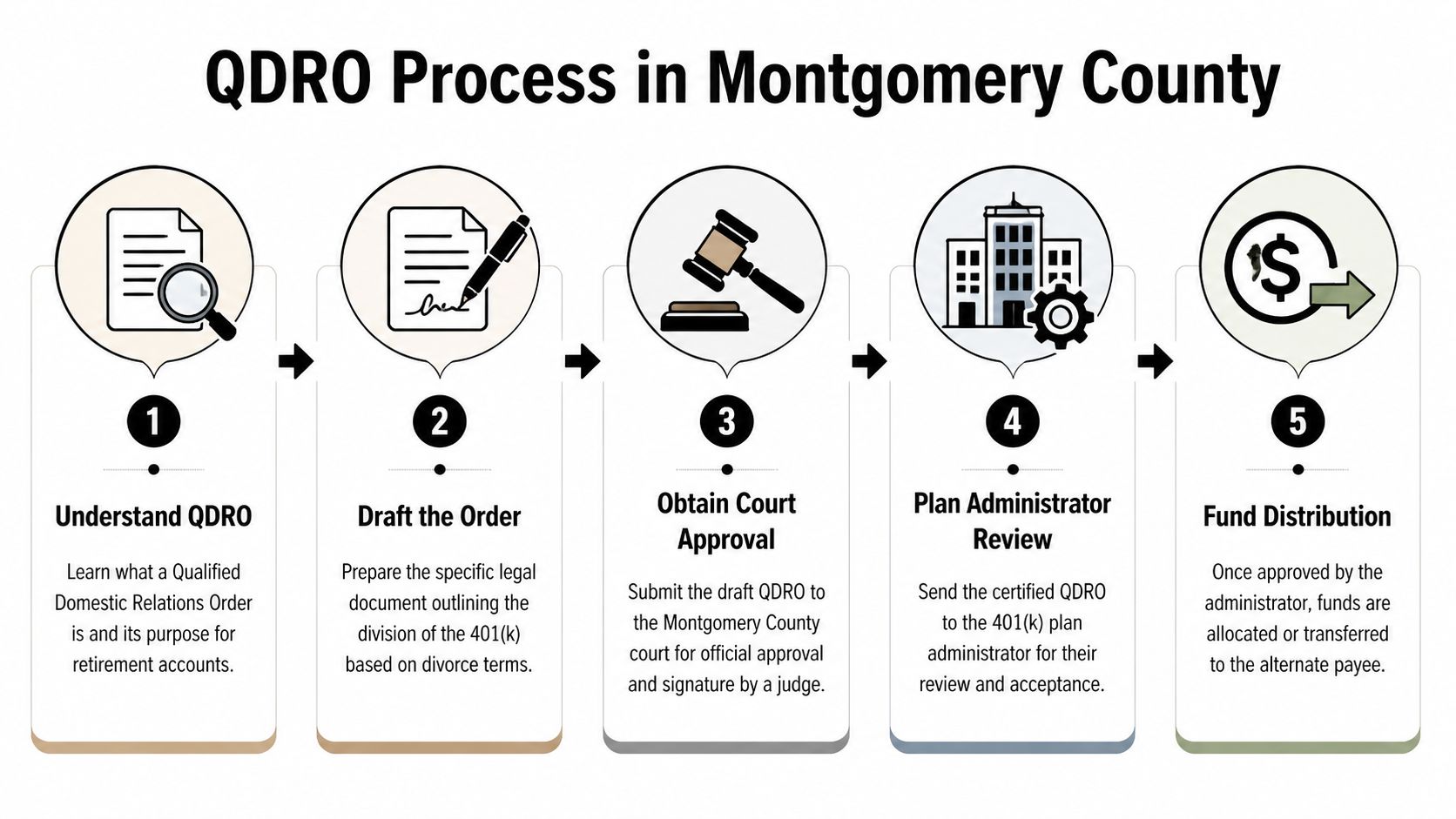

Executing the QDRO Process in Montgomery County

A common Woodlands divorce problem looks like this: the final decree is signed, everyone believes the 401(k) issue is over, and then the plan administrator rejects the transfer paperwork. Months pass. The account keeps moving with the market. One spouse wants answers, and the other assumes the delay is the court's fault.

Usually, the problem is not the decree. It is the missing or poorly drafted Qualified Domestic Relations Order, or QDRO.

For most employer retirement plans, the decree says what the parties agreed to or what the judge ordered. The QDRO is the separate order that tells the plan exactly how to divide the account. If the decree awards 50 percent of the community portion, but the QDRO does not define that share clearly, address gains and losses, and match the plan's rules, the transfer can stall.

What a QDRO has to accomplish

A usable QDRO does four jobs at once. It identifies the correct participant and alternate payee, names the correct plan, states the division formula with enough precision for the administrator to apply it, and stays consistent with both the decree and the plan's written procedures.

That last part causes many of the headaches.

A judge in Montgomery County can sign an order that still gets rejected by the plan because the plan administrator is not checking whether the language sounds fair. The administrator is checking whether the order complies with ERISA, the plan document, and the plan's internal processing rules. That is why plan-specific drafting matters. For a closer explanation of how retirement-plan language and divorce orders fit together, see this guide on divorce with retirement accounts in The Woodlands.

How the process usually works in Montgomery County

The smoothest files usually follow the same sequence.

Get the plan information before drafting anything.

The summary plan description, plan name, model QDRO language if the administrator offers it, and distribution rules should be in hand before anyone starts writing.Draft the QDRO to the actual plan.

Generic templates cause avoidable problems. I see issues with the wrong plan title, no gains-and-losses language, no valuation date, and terms that conflict with the decree.Ask for preapproval if the plan allows it.

Some administrators will review a draft before the judge signs it. That step often saves time because errors get fixed before the order goes to court.Get the order signed through the Montgomery County court handling the divorce.

In practice, that usually means presenting the QDRO to the same court that signed the final decree, whether it is signed with the decree or shortly after. Local procedure is usually manageable. The larger risk is assuming the court signature finishes the job.Send the signed order to the plan and track implementation.

Someone has to confirm receipt, respond to any deficiency notice, and verify that the account was divided.

A signed decree without an accepted QDRO does not transfer retirement money.

Where Woodlands cases often go sideways

The mistakes are usually ordinary, not dramatic. The wrong employer may have been listed instead of the formal plan name. The decree may award a share of the community portion, while the QDRO states a flat percentage of the full balance. The order may leave out what happens to gains and losses between the valuation date and the date of division.

Another recurring problem starts earlier, at valuation. If the underlying math is wrong, the QDRO carries that mistake forward. In Montgomery County cases with premarital balances, stock market growth, loans, or years of contributions, the subtraction method often creates false confidence. It is fast, but it can overstate the community share because it fails to track growth on the separate portion correctly. That mistake can affect the full property division, especially when one spouse is weighing a retirement split against keeping more home equity.

A real trade-off clients miss

Clients sometimes focus so heavily on getting the QDRO signed that they miss the larger strategy question. If the account division is based on weak tracing or vague decree language, the QDRO stage becomes expensive cleanup. It is much cheaper to define the community share correctly before the decree is signed than to fight over wording after.

That matters in Montgomery County because many cases settle in mediation with broad language such as "Wife is awarded 50 percent of the community interest in Husband's 401(k)." That can be workable. It can also create a dispute later if nobody defined the valuation date, gains and losses, outstanding loan treatment, or whether the account includes a premarital component that was never traced properly.

Common reasons a QDRO gets rejected

- Wrong plan name or wrong plan type

- Terms that do not match the decree

- No clear formula or valuation date

- No language for gains and losses

- Missing plan-specific elections or procedural requirements

- Drafting based on flawed community-property math

As noted earlier, plan administrators are more likely to approve orders that are drafted from the actual plan documents and reviewed before submission. The same source also warns that generic drafting, skipped preapproval, and incorrect valuation methods can lead to rejection, delay, and expensive tax problems if someone tries to move funds without a proper order (peacockesq.com QDRO guide).

Why follow-up matters as much as drafting

After the judge signs, someone still has to finish the file. Certified copies may be needed. The administrator may request revisions. The employer may change recordkeepers. A participant may leave the job before the order is processed. Every one of those issues can slow distribution.

This part gets overlooked often. In a busy divorce docket, a signed order feels like closure. For retirement accounts, closure happens when the plan accepts the order and completes the transfer. Until then, the case is still alive in a very practical sense.

Negotiating Your 401k Share vs Going to Court

You sit down for mediation in The Woodlands expecting a simple 50-50 split. By the end of the first hour, the primary question is different. Should the 401(k) be divided at all, or is it better used to solve a bigger property problem?

Mediation gives you options that court may not

In Montgomery County, many retirement disputes settle in mediation because spouses can trade assets instead of forcing a direct split of every account. A 401(k) can be offset against home equity, cash, brokerage funds, or another asset if the overall division still makes sense.

That flexibility matters. A spouse who wants to keep an intact retirement account may be willing to give up more equity in the house. Another spouse may prefer cash access or a cleaner break from the marital home instead of waiting on retirement funds.

The hard part is valuation. Home equity, retirement money, and taxable investment accounts do not carry the same after-tax value. A pre-tax 401(k) balance usually should not be treated as equal to the same dollar amount in cash or equity. Clients also need to avoid the common subtraction method, where someone merely subtracts the account balance at marriage from the balance at divorce and calls the difference community property. In a Montgomery County case, that shortcut can produce bad numbers fast if there were loans, rollovers, employer matches, or market gains on a separate-property component.

What usually makes settlement stronger

An offset often makes sense in cases like these:

- The house has substantial equity and one spouse wants to stay in it.

- There is a credible separate-property claim tied to premarital contributions, and neither side wants to spend more on tracing fights than the issue is worth.

- The plan is difficult to divide because the employer or administrator adds delay, extra review, or restrictive procedures.

- The spouses need different things. One needs liquidity or housing stability, while the other wants long-term retirement growth.

I often tell clients to compare function, not just face value. A house solves one problem. A 401(k) solves another. Trading one for the other can be smart, but only if the numbers are adjusted accurately and the decree is drafted to match the deal.

Court puts the decision in the judge's hands

If settlement fails, the Montgomery County court will divide the community estate under Texas Family Code § 7.001 using a just-and-right standard. That does not promise an exact half. It gives the judge room to weigh the full facts of the marriage.

That matters in cases involving fault, a large earnings gap, health problems, waste of assets, reimbursement claims, or parenting arrangements that affect one spouse's financial future. In those files, going to court can help or hurt, depending on the evidence. A spouse asking for more than half needs proof, not suspicion. A spouse expecting a neat 50-50 result should understand that judges are not required to give one.

Local procedure also affects strategy. In Montgomery County, mediation often happens before trial settings tighten, and judges expect the property issues to be narrowed as much as possible before final hearing. If the 401(k) becomes the last disputed asset, the legal fees spent fighting over it can outweigh the value gained by pressing for a slightly better percentage.

A practical comparison

| Path | Benefits | Risks |

|---|---|---|

| Negotiated offset | More control over the final package, fewer retirement-plan moving parts | Bad math can leave one spouse with less real value than expected |

| Direct 401(k) split | Works well when the share and valuation method are clear | Still requires careful drafting and follow-through |

| Court decision | Useful when one spouse is hiding information or refusing reasonable terms | Higher cost, less control, and a judge may value the facts differently than you do |

One more point gets missed often. If you are trading a 401(k) against another asset, tax treatment has to be part of the conversation before you sign. The wrong offset can look fair on paper and turn out lopsided after taxes, basis, or withdrawal rules are applied. That is why many clients benefit from reviewing the proposed split with counsel familiar with both divorce property division and related tax issues in Woodlands family cases.

A good settlement does not just divide numbers. It solves the right problem, uses reliable valuation, and avoids a fight that costs more than it is worth.

Avoiding Costly Tax and Penalty Traps After the Split

A common Woodlands divorce problem looks like this. The decree is signed, everyone assumes the retirement piece is done, and then a spouse takes money out the wrong way, misses a plan deadline, or learns the administrator rejected the order. The case may be over in court, but the tax damage starts after that.

A 401(k) division is only safe if the transfer happens through the plan's required process and the paperwork matches the decree. In Montgomery County, I tell clients to treat post-decree retirement work as its own file. Follow up with the plan administrator. Confirm approval in writing. Make sure the account is divided before anyone acts as if the money is freely available.

A signed decree does not finish the tax analysis

The biggest mistake is assuming the decree alone protects you. It does not. The plan administrator follows the QDRO and the plan rules, not the parties' assumptions about what should happen.

That matters for taxes and timing. A transfer made under a proper QDRO is treated differently from an ordinary early withdrawal. If the receiving spouse wants to keep the funds invested for retirement, a direct rollover into an IRA or other eligible account is often the cleaner path. If the receiving spouse needs cash, the tax bill still has to be part of that decision, even if the early withdrawal penalty is avoided through the QDRO process.

This is also where bad settlement math shows up. A spouse may agree to take more home equity and less 401(k), or the reverse, without pricing in taxes, liquidity, refinance risk, and the cost of carrying the house after divorce. On paper, those trades can look even. In real life, they often are not.

Two choices after the transfer

Once the awarded share is ready to move, the receiving spouse usually has two options.

- Take a distribution. This may provide needed cash for rent, legal bills, or a fresh start, but income taxes can reduce what is available.

- Complete a direct rollover. This usually preserves more long-term value and avoids turning a property division into an immediate tax event.

The right answer depends on the rest of the property division. A spouse keeping the home may need liquidity more than retirement growth. A spouse with stable housing and income may be better served by preserving the account. The point is to make that choice deliberately, not by default.

If the divorce involves larger assets, offsets, or questions about withdrawal treatment, it helps to review the plan with counsel who handles tax law issues tied to divorce property division.

Details that cause expensive problems

Two issues get missed often in Montgomery County cases.

- 401(k) loans: An account statement can overstate what is really there if a plan loan is outstanding. The decree and QDRO should make clear who bears that loan and how it affects the division.

- Beneficiary designations: The divorce does not reliably update every beneficiary form on file with the employer or plan. Those forms should be reviewed and changed promptly after the divorce.

One more caution. If part of the account was separate property before marriage, do not fall back on the subtraction method when you evaluate what was divided or what remains. Investment gains and losses tied to the separate portion matter. Loose math in this area creates tax and property disputes that are harder to fix after entry of the final decree.

Here is a helpful overview before making a withdrawal or rollover decision:

What to avoid after the divorce

Do not ask payroll to split the account informally. Payroll is not the decision-maker.

Do not cash out because the process feels slow. A rushed distribution can create taxes that were never part of the bargain.

Do not assume the administrator accepted the QDRO just because it was signed by the judge. In practice, some of the longest delays come from orders that looked fine in court but did not match plan requirements.

The safer approach is plain and boring. Confirm the order was submitted. Confirm it was approved. Confirm when the transfer will occur. Then decide whether to roll the funds over or take a distribution with the tax consequences fully understood.

What to Do Next A Checklist for Your Woodlands Divorce

A common Woodlands divorce problem looks like this. One spouse wants to keep the house because the children are settled there. The other is willing to trade equity for a larger share of the 401(k). That trade can work, but only if the numbers are grounded in records, tax consequences, and a realistic timeline for getting a QDRO approved.

This is the stage where small mistakes become expensive. A rough estimate of the account balance is not enough. A casual agreement to "subtract the premarital amount" is not enough either, especially if part of the 401(k) existed before marriage and the account rose or fell over time. In Montgomery County cases, I want clients to get organized before mediation, not after, because judges expect the decree and retirement language to match what can be enforced.

What to do next

- Collect the right statements: Get 401(k) statements from the date of marriage through the most recent available date. If the account existed before marriage, get the statement closest to the wedding date and any year-end statements that help trace gains and losses.

- Get the plan's rules in writing: Ask the plan administrator for the Summary Plan Description, loan information, beneficiary information, and any sample or model QDRO language.

- Build a property spreadsheet: List the house, mortgage balance, retirement accounts, bank accounts, vehicles, stock, restricted units, debts, and any business interests. This is how you compare a retirement division against a buyout, refinance, or home equity trade.

- Value assets with taxes in mind: A dollar in a 401(k) is not the same as a dollar in cash or home equity. If you are discussing offsets, account for taxes, penalties where applicable, and liquidity.

- Identify loans against the plan: An outstanding 401(k) loan changes the actual value of the account and can complicate settlement language.

- Review beneficiary designations after the divorce is final: Do not assume the plan or employer updates those forms for you.

- Raise fault, reimbursement, and custody facts early: In Texas, those facts can affect a just and right division. They should shape strategy before settlement positions harden.

- Ask for a tracing plan if separate property is claimed: The burden of proof matters. So does the method used. Do not rely on the subtraction method where investment performance on the separate portion must be addressed.

- Use plan-specific QDRO drafting: Court approval is only part of the job. The plan administrator still has to accept the order.

- Set a pre-mediation review with your lawyer: Before mediation, decide whether you want retirement funds, more home equity, or a mix. Each option has different risks for taxes, timing, and post-divorce cash flow.

- Prepare for Montgomery County procedure: Make sure the decree language, QDRO language, and supporting records are ready in the right sequence. Delays often happen because one document says one thing and the retirement order says another.

One practical point matters more than clients expect. If you are the employee spouse and part of the account is separate property, prove it with records now. If you are the non-employee spouse, do not accept a spreadsheet that treats premarital contributions like a simple subtraction problem. That shortcut often ignores growth, losses, and plan activity during the marriage.

For readers comparing options, firms that handle Montgomery County family law matters, including retirement account division, can help evaluate tracing, QDRO drafting, and settlement structure. One example is The Law Office of Bryan Fagan, which serves The Woodlands and surrounding communities in divorce and property division matters.

This article is for informational purposes only. It is not legal advice. The right approach depends on your plan, your records, your decree language, and the facts of your case.