You may be sitting in the house right now, looking at the kitchen table, the mortgage statement, and the kids’ backpacks by the door, wondering the same thing most Montgomery County clients ask early in a divorce: What happens to the house?

For many families in The Woodlands, the house is the largest asset in the marriage and the hardest one to divide. It’s also where emotion and math collide. One spouse wants stability for the children. The other wants access to equity and a clean financial break. Both may be worried about whether anyone can afford the property on one income.

Texas law gives you a starting point, but not a simple answer. Under the Texas Family Code, courts divide the marital estate in a manner the court considers just and right. That sounds straightforward until you add mortgage debt, refinancing problems, separate property claims, and local housing realities in Montgomery County.

Housing decisions after divorce often force major lifestyle changes. One survey reported that 53% of people downsize after divorce according to the Institute for Divorce Financial Analysts. That tracks with what we see in practice. Even when someone wants to keep the home, wanting it and being able to carry it are two different things.

Your Home and Your Divorce What Montgomery County Residents Need to Know

A common local situation looks like this. A couple in Alden Bridge or Sterling Ridge has built years of equity, but their mortgage payment still reflects an older loan. One spouse assumes the house should be sold. The other assumes the court will let them stay because the children are settled in school. Both assumptions can be wrong.

In Montgomery County, the house is usually part legal issue, part finance issue, and part timing issue. The deed matters. The mortgage matters. The children matter. So does whether a lender will approve a refinance after support, legal fees, and other debts are factored in.

The first question is usually not who wants the house

It’s whether the house is community property, separate property, or mixed. That analysis affects whether the equity gets divided, whether one spouse has a reimbursement claim, and what options are realistic.

A second question comes fast behind it. If one person keeps the house, how will the other person get paid and removed from financial risk?

Practical rule: The house doesn’t get divided on sentiment alone. It gets divided through title records, loan documents, valuation, and a workable plan.

Montgomery County courts also tend to focus on practical outcomes. If minor children are involved, judges often give serious weight to stability. But stability doesn’t override affordability. A parent who can’t qualify for the home long term may still end up facing a sale, even if everyone agrees it would be better for the children to stay put.

Local reality in The Woodlands

Generic internet articles often skip the issue that matters most here. In higher-value neighborhoods, the equity may look strong on paper, but the path to converting that equity into a buyout can be difficult. That’s especially true when one spouse is trying to keep a house after the divorce on a single income.

Consequently, what happens to the house in a divorce usually comes down to one of a few practical paths. Before you choose one, you need to know what kind of property interest you’re dealing with.

Is the House Community or Separate Property in Texas

Texas starts with a basic split. Property acquired during marriage is usually presumed to be community property under the Texas Family Code. Property owned before marriage, or acquired by gift or inheritance, may be separate property.

That sounds simple until real life gets involved.

Think of it like two jars

One jar is personal. That’s separate property. The other jar is shared. That’s community property.

If a spouse owned the house before marriage, that house may begin in the personal jar. But if marital earnings are later used to pay down the mortgage or improve the property, the shared jar may gain a claim against the home. That doesn’t always convert the entire house into community property, but it can create a reimbursement or equitable claim that matters a lot in settlement negotiations.

Hybrid homes create the biggest fights

This issue comes up often in Creekside Park, Carlton Woods, and other parts of The Woodlands where a spouse brought a house into the marriage and the couple later treated it like the family home.

When marital funds are used to reduce the mortgage on a premarital home, the non-titled spouse may have a claim to part of that equity. In contested cases with proper tracing, non-titled spouses can recover 20% to 40% of that hybrid equity according to LaFrance Law’s discussion of divorce and the house.

That claim usually depends on records. Bank statements, mortgage histories, renovation invoices, and account sourcing often matter more than either spouse expects.

- Premarital ownership helps, but it isn’t the end of the story: If one spouse bought the home before marriage, that supports a separate property argument.

- Marital payments can create a claim: Community income used to reduce principal or fund improvements may give the other spouse a reimbursement position.

- Commingling makes proof harder: If accounts were mixed for years, tracing becomes central.

- Paperwork wins these disputes: We often tell clients to gather closing papers, refinance records, and proof of where improvement money came from before negotiations begin.

A house can be separate in origin and still produce a community reimbursement issue by the time of divorce.

If you’re facing that kind of mixed-property question, our page on property division in a The Woodlands divorce gives a broader overview of how these claims are analyzed.

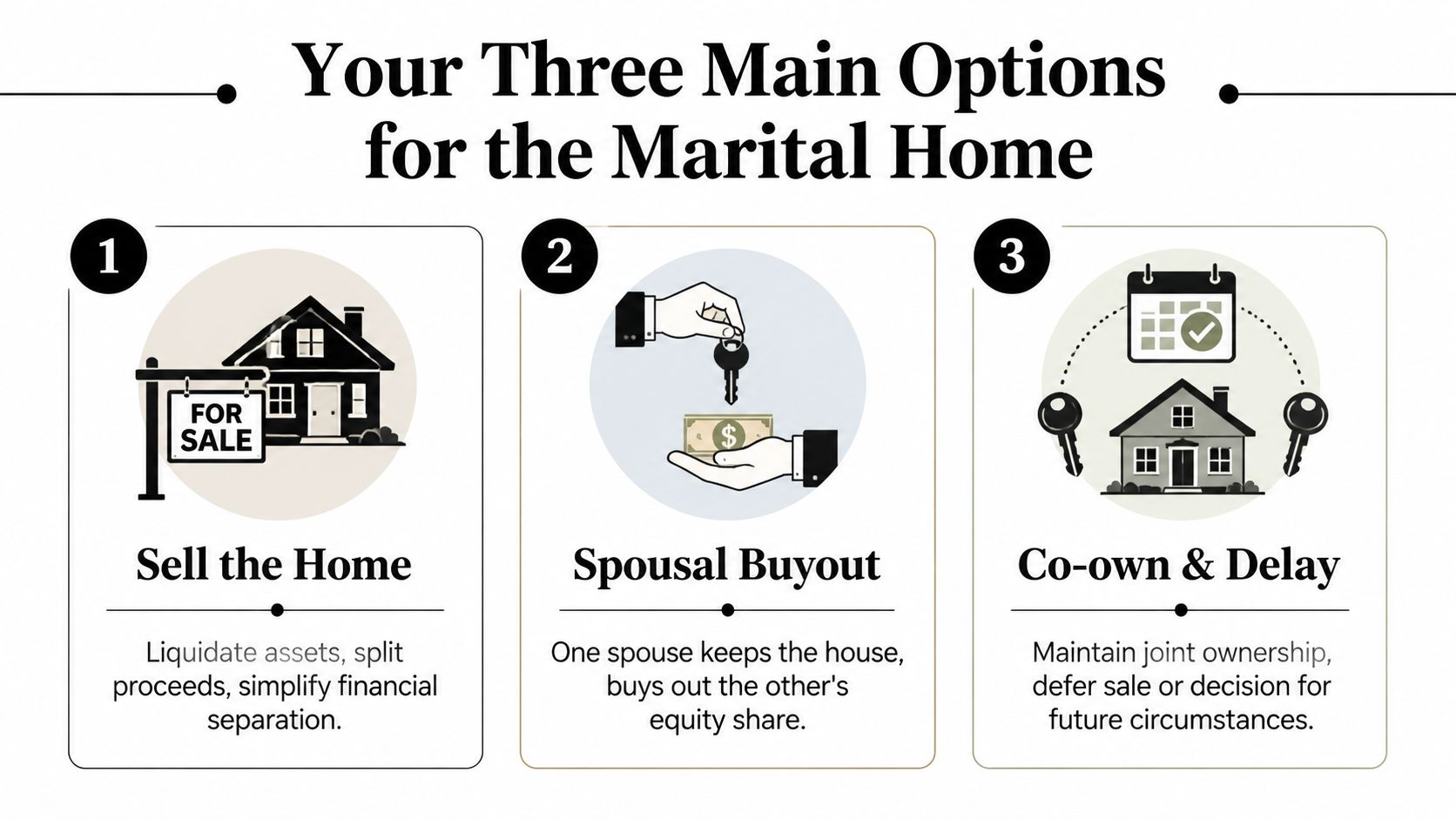

Your Three Main Options for the Marital Home

Once the home is identified as marital or partly marital, the next issue is practical. What are you going to do with it? In most Texas divorces, the answer falls into one of three working options.

A licensed appraiser typically determines the home’s current market value first, then the court or the parties use that value to structure division. Common methods include sale, buyout through refinancing, continued co-ownership, or a deferred sale according to Experian’s explanation of home equity division in divorce.

Option one, sell the home

Selling is usually the cleanest option when neither spouse can comfortably carry the home alone.

It ends shared ownership, pays off the mortgage, and converts the house into cash that can be divided under the settlement. It also limits future fights about repairs, taxes, insurance, and missed payments.

The downside is obvious. It forces a move, and if children are involved, that can be disruptive.

Option two, one spouse buys out the other

This is the option many people want. One spouse keeps the house and pays the other for their share of equity, often through refinance proceeds or by offsetting other assets.

It can work well when a parent wants to keep the children in the same school zone and can qualify for financing. It works poorly when the plan depends on hope instead of lender approval.

A lot of people start searching for ways to shift mortgage responsibility informally. Resources on topics like passing a home loan to family can help people understand loan transfer issues generally, but in divorce cases the better question is usually whether the lender will approve a refinance or assumption tied to the decree.

Option three, co-own and delay the final sale

Some couples agree to keep joint ownership for a period of time. One spouse stays in the house, often while children are young, and the home is sold later.

This can preserve stability in the short term. It also creates ongoing ties after the divorce, which many people underestimate. Co-ownership requires detailed written terms on possession, repairs, insurance, taxes, payment deadlines, and the triggering event for sale.

Comparing Your Options for the Marital Home

| Option | Best For… | Key Challenge | Financial Outcome |

|---|---|---|---|

| Sell the Home | Couples who want a clean break and immediate liquidation | Moving on a deadline and agreeing on sale logistics | Net proceeds are divided under the decree |

| Spousal Buyout | Families trying to keep children in the home and school pattern | Qualifying for refinance and funding the buyout | One spouse keeps the house and the other receives an equity offset or payout |

| Co-own and Delay | Cases where immediate sale or refinance isn’t practical | Ongoing conflict, unclear maintenance duties, delayed final separation | Equity division is postponed until a later sale or trigger event |

Key takeaway: The best option isn’t the one that feels least painful today. It’s the one the parties can actually perform after the decree is signed.

Real-World Scenario A Buyout in Sterling Ridge

Sarah and Tom live in Sterling Ridge. They have children in local schools, and both agree that uprooting them during the divorce would make an already hard year worse. Sarah wants to keep the house. Tom wants his share of the equity and a complete release from the mortgage.

That sounds like a standard buyout. It usually isn’t.

How the process usually unfolds

First, they get a formal appraisal so everyone is working from the same number. That avoids the common problem of one spouse relying on an optimistic online estimate while the other relies on a lower private opinion.

Next, the lawyers calculate the equity position and decide how Tom’s share will be paid. In Texas, one tool that may be used in the right case is an Owelty Lien. In practical terms, it can help structure a lien against the property to secure one spouse’s equity interest as part of the division.

Where cases get stuck

The hard part is often not reaching the agreement. The hard part is carrying it out.

Sarah may be able to make the current payment, but that doesn’t mean she’ll qualify for a new loan in her sole name. Lenders review income, debt, support, and credit under their own underwriting rules. If she can’t refinance within the deadline set in the decree, the parties may be pushed back toward sale even after they thought the issue was resolved.

That’s why we try to test the financing path early. A buyout is strongest when the person keeping the home has already spoken with a lender, understands the payment range, and knows what documents will be required.

Why local planning matters

In Montgomery County, judges generally want decrees that can be enforced without future chaos. A decree that says one spouse “will refinance later” without hard dates, lien language, deed language, and a backup sale provision often creates post-divorce conflict.

Sarah and Tom’s scenario is fictional, but the structure is familiar. The successful buyouts are usually the ones built around lender reality, not just family preference.

Dealing with the Mortgage and Protecting Your Credit

Many divorcing spouses think the decree alone solves the mortgage problem. It doesn’t.

A divorce court can assign responsibility between spouses, but the lender is not bound by your decree unless the loan is refinanced, assumed if allowed, or paid off. That gap is where credit damage happens.

A quitclaim deed is not a mortgage release

This is one of the most expensive misunderstandings in divorce.

A quitclaim deed transfers ownership interest, but it does not remove a spouse from the mortgage obligation. The spouse who signs away title can remain liable on the loan and can still suffer credit harm if the other spouse misses payments, as explained in this discussion of divorce, title transfer, and mortgage liability.

That means an “out-spouse” can end up with no ownership and still have loan exposure. From a credit standpoint, that is a bad result.

What usually works better

The cleaner solution is refinance into the retaining spouse’s sole name. If that can’t happen immediately, the decree needs more than vague promises.

In Texas property practice, attorneys may also use tools such as special warranty deeds, deeds of trust to secure assumption, lien language, deadlines, and sale triggers. The exact documents depend on the case, the lender, and whether the parties are dividing community property, securing reimbursement, or handling a buyout.

If you’re also dealing with title issues, deed questions, or transfer paperwork, our overview of real estate law services in The Woodlands can help frame the property side of the problem.

Don’t sign away title unless you understand whether your name is still attached to the debt.

Timing matters more than many people expect

The current lending environment has made this harder for single-income borrowers. One legal analysis on rising rates and divorcing homeowners notes that mortgage rates above 6% can raise monthly payments by hundreds compared with earlier low-rate loans, making a buyout much harder after divorce expenses and income changes, as discussed in Curran Moher’s article on rising rates and divorcing homeowners.

That’s why we often urge clients to talk to a lender before final mediation, not after. If the retaining spouse won’t qualify, it’s better to know that while options are still open.

This short video gives a useful overview of why mortgage planning and divorce orders have to line up:

Credit protection steps that matter

- Check the actual loan status: Confirm whose names are on the note, not just on the deed.

- Get lender input early: Ask whether refinance, assumption, or payoff is the realistic path.

- Set deadlines in the decree: Open-ended mortgage provisions tend to create enforcement disputes.

- Build a backup plan: If refinance fails, the decree should address sale procedures.

Who Stays in the House During the Divorce

This question comes up early, often before anyone is ready to decide the final property split. In Montgomery County, that issue is usually addressed through temporary orders.

A judge can award one spouse temporary exclusive use of the house while the case is pending. If children are involved, the court often looks closely at stability, school routines, and the day-to-day caregiving pattern. The controlling framework in Texas is still the Texas Family Code, especially the court’s authority to enter temporary orders while the divorce is underway.

Exclusive use is temporary, not final ownership

Living in the home during the case doesn’t mean you’ll receive the house in the final decree.

Temporary possession is often about reducing disruption and preserving order while the divorce moves forward. It can also be tied to who is paying the mortgage, who is caring for the children most of the time, and whether conflict in the home has become unworkable.

If you want to understand how those hearings work locally, this page on a temporary orders hearing in Montgomery County divorce cases gives a practical overview.

The overlooked issue of rental value credit

There’s another concept many people never hear about until late in the case. A spouse who moves out can sometimes argue for a rental value credit against the spouse who had exclusive use of the home during the divorce.

According to this analysis of rental value credit claims in divorce housing disputes, the idea is that exclusive use of the property may justify an offset in final division based on fair market rental value, and in areas like The Woodlands that can amount to thousands per month.

If one spouse had the benefit of sole use for a long period, it may be worth asking whether that benefit should be accounted for in the final numbers.

This isn’t automatic. It has to be raised, supported, and evaluated in the context of the case. But in the right Montgomery County divorce, it can be an important fairness argument.

What to Do Next A Checklist for Your House and Divorce

The house issue usually turns on paperwork and cash flow, not instinct. In Montgomery County, we see people get into trouble when they wait too long to collect records, assume a refinance will be easy, or agree to a house deal before they know what they can afford at current interest rates.

A practical checklist

- Pull the key records first: Get the deed, latest mortgage statement, home equity loan paperwork, tax records, insurance declarations page, and any HOA documents.

- Confirm how and when the property was acquired: Closing papers, refinance documents, and proof of premarital ownership can shape a separate property or reimbursement argument.

- Collect proof of payments: Bank statements, canceled checks, and escrow histories matter if one side claims community funds were used to reduce principal, pay for repairs, or improve a separately owned house.

- Get a realistic value, not a guess: A local market estimate is a start, but an appraisal is often the number that drives settlement.

- Talk to a lender early: Ask what a refinance would require on one income, whether debt-to-income ratios work, and what payment would look like in the current rate environment.

- Run the full monthly cost: Include taxes, insurance, HOA dues, utilities, routine upkeep, and likely repairs. Many buyouts fail because people only look at principal and interest.

- Review the equity gap: If one spouse wants to keep the house but cannot pay a lump sum, ask whether an Owelty Lien may be part of the solution.

- Document child-related housing concerns: If staying in the home ties directly to school attendance, transportation, or parenting time, write down the specific facts.

- Separate title from loan liability: Signing over a deed does not remove a name from the mortgage.

- Set a fallback plan now: If the refinance is denied or delayed, decide how a listing, price reduction, possession, and sale proceeds would be handled.

- Get the agreement into enforceable language: Vague side promises about the house create expensive disputes later.

If selling or downsizing is likely

Selling the home is often the cleanest option on paper, but the practical side can be hard, especially after years in one place. A guide to clutter-free downsizing can help you plan the move while the legal pieces are still being worked out.

One final caution

This article is general information for people in The Woodlands and Montgomery County, Texas. The right answer in your case depends on title history, loan terms, available equity, and whether the court is looking at a refinance, sale, or lien-based buyout structure. If a death in the family affects ownership, the Texas Estates Code may also affect title and the steps required before the property can be divided.